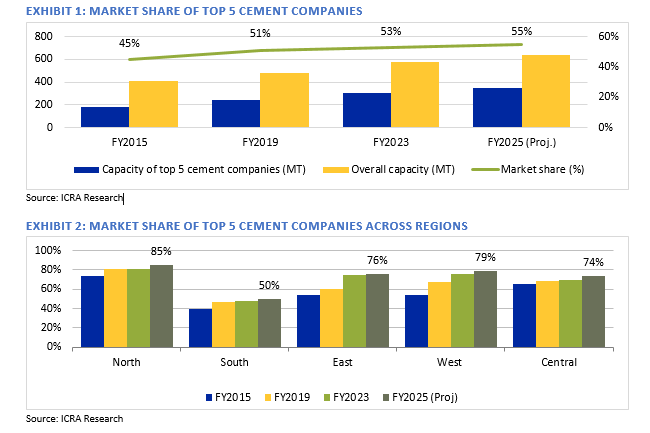

Market share of top five cement companies expected to increase to 55% by March 2025: ICRA

Lenders’ haircut for cement sector under IBC stands at 21% compared to overall average of 68%

Backed by healthy demand prospects for the cement sector, large cement companies are looking to increase their capacity and maintain market share through organic and inorganic expansions. ICRA estimates that the market share of the top five cement companies witnessed a steep rise to 54% as of December 2023 from 45% as of March 2015, and expects it to further increase to 55% by March 2025, resulting in consolidation in the cement industry. Except the ACC and Ambuja acquisitions by the Adani Group, other mergers and acquisitions (M&As) were largely owing to the cash flow-starved nature of the acquired entity or the group’s financial stress.

Giving more insights, Anupama Reddy, Vice President and Co-Group Head, Corporate Ratings, ICRA, said: “While organic growth is expected to continue in the medium term, cement companies are also preferring the inorganic route to boost capacities rapidly, leading to consolidation in the industry. There were 15 M&As in the last nine years in the cement industry with the average cost of the M&A ($80/MT) being lower than the cost of setting up an integrated greenfield cement plant ($110–120/MT), thus leading to capex cost savings. This further entails access to readymade capacity, limestone reserves and prevents companies from the hassle of longer gestation periods for stabilisation of operations in case of a greenfield unit. Asset block of 28 MT is in pipeline for acquisition and ICRA expects M&A deals to continue, given the aggressive growth plans of the large incumbent players who want to maintain their market share.”

The bulk of the cement produced within a region is usually consumed internally and the excess transported to adjacent regions. The consolidation, taking place across India, is primarily led by the eastern and the western regions. The share of the top five cement companies in the eastern and the western regions is estimated to increase to 76–79% in FY2025 from 54% in FY2015. The southern region is highly fragmented with only 40% share held by the top five cement players in FY2015. This may go up to 50% by FY2025. The northern and central regions were highly consolidated in the past (~65-75% in FY2015) and are expected to remain in the range of ~75-85% by FY2025.

Till March 31, 2024, 947 corporate insolvency cases across the sectors were resolved under the Insolvency and Bankruptcy Code (IBC) with an average haircut of 68%. However, the average haircut through the IBC route for the cement sector stands at 21%, which is much lower than the overall average. The primary reasons working in favour of brownfield acquisitions have been access to good quality limestone reserves and higher cost of setting up greenfield cement plants compared to the acquisition of existing operational ones.

“ICRA expects the credit profile of cement producers to remain stable, driven by a healthy growth in operating income, improvement in operating margins and comfortable leverage metrics. Although the debt dependence is likely to remain high to fund the ongoing capex plans, the leverage metrics of the cement companies[1], as measured by Total Debt/OPBIDTA, are estimated to remain comfortable at 1.3-1.4x in FY2025 compared to 1.4-1.5x in FY2024. Consequently, the coverage metrics are expected to remain healthy with DSCR at 2.7-2.8x, supported by an improvement in OPBIDTA in FY2025,” Reddy added.